You can still track financial statements, types of audit reports you can issue besides unqualified taxes, payroll, customers, and vendors, but the amount of report templates is much more limited. And just like QuickBooks, payroll insights are only available with a paid add-on. Professional, customizable invoices that are quick and easy to create.

Pricing

Important to note is that if you decide to use the trial, you are no longer eligible for the 50% discount for your first three months. We will give this round to Wave since it offers basic software for free, and if you wish to go with add-ons, they also fall into the reasonably priced range. If there are ever book reconciling items that have not yet been recorded, you can save the reconciliation for later while you add missing book entries. Aside from bank reconciliations, you can print checks in QuickBooks. If you’re still open to other solutions, our handy comparison table will help you whittle down the competition in minutes. Includes audit trails and easy accountant access; has millions of users so your accountant will likely be familiar with it.

Wave and QuickBooks Online alternatives

The hourly cost rate calculator provides a clear idea of how much you’re paying on employee wages and taxes. However, each tool offers different methods for tracking finances and staying on top of your books. By providing feedback on how we can improve, you can earn gift cards and get early access to new features. Another useful feature is ordinary annuity definition a real-time sync between QuickBooks mobile and QuickBooks online, enabling data consistency across all devices. When it comes to pricing, both solutions offer several different options ranging from affordable to more expensive, depending on your needs and the number of users. Only integrates with in-house apps, like Wave Payments and Wave Payroll; does not integrate with card readers for in-person payments.

Just like Wave Accounting, though, Wave Payroll is cheaper than QuickBooks Payroll. Its self-service plan costs $20 a month plus an additional $6 per employee. And its full-service plan is just $35 a month, which puts it on the lower end of the payroll-cost spectrum. (QuickBooks Payroll sales pricing starts at $37.50 a month plus $5 per payee—which honestly could make it cheaper than Wave Payroll depending on the number of employees you have).

However, if you’re just managing a budding business or something on the side, Wave’s minimal feature set won’t set you back too much. Even better, its free software has features many other accounting solutions charge extra for. For instance, Xero’s cheapest plan limits you to 20 invoices a month—if you want unlimited invoices, you’ll need the $34 a month Growing plan. Includes project tracking tools in higher tier plans; has transaction tracking tags; lacks industry-specific reports; users with multiple businesses must pay for separate subscriptions. Has robust reporting tools and report customization options, invoicing for an unlimited amount of clients, inventory tracking in higher tier plans, plus a capable mobile app. The more advanced time tracking app, QuickBooks Time, is only available if you pay for QuickBooks Payroll, which comes at an additional cost.

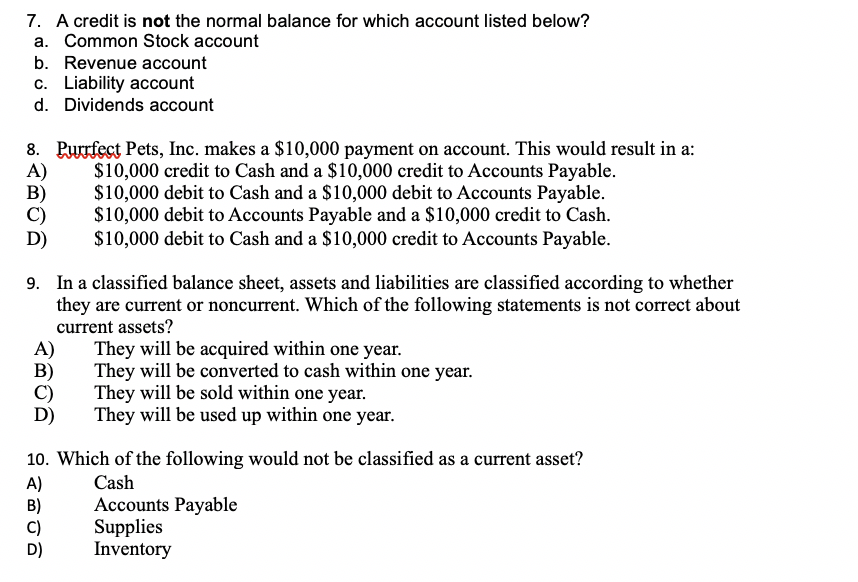

There are three different plans to choose from, based on the needs of your business. The Core plan is the least expensive and includes full-service payroll. The Premium plan adds more features, such as workers’ comp administration and same-day direct deposit. The top-level Elite plan gives you access to features, including a personal HR advisor, customized setup, and 24/7 customer support.

QuickBooks boasts significantly more features than Wave

It’s important to note Wave won’t have specific QuickBooks accounting history, so you should keep a copy of old transactions for your records. With QuickBooks, you can enter your location, and compare tax considerations by business type QuickBooks will figure out the requirements for your area. But when I went to configure it, the app booted me out of my invoice draft and I lost all my work. The extra cash you shell out for QuickBooks translates into a whole gamut of extra features. So not only do you get your money’s worth, but these features also help support the complex needs of larger businesses.

Time-saving features like scheduled payment reminders and automatic credit card payments.

For instance, Xero’s cheapest plan limits you to 20 invoices a month—if you want unlimited invoices, you’ll need the $34 a month Growing plan.

When I was 10 years old, I had a small business that involved going door to door with an empty ice cream pail and a can-do attitude to sell my dog doo-doo disposal services.

When it comes to affordability, there really is no contest —Wave offers better value than QuickBooks.

Today’s leading accounting platforms offer standard security features like data encryption, secure credential tokenization and more.

The Best Corporate Credit Cards For Businesses

While QuickBooks remains the number one choice for larger businesses with specific accounting needs, Wave shouldn’t be discounted entirely. However, it’s important to note that lots of QuickBooks’ enhanced tools, like stock handling and project profitability, are reserved for its pricier tiers. QuickBooks has a much stronger accounting toolkit, offering users a much wider selection of useful features than Wave. However, this doesn’t mean Wave should be ruled out, as the software’s feature package performed particularly well in our last round of testing.

After that, you can input all your products or services and have the option to add pictures, stock quantity, vendor information, and more. QuickBooks includes an option to add on accounting, which adds bill management, inventory and job costing capabilities in addition to expense tracking. The platform also includes receipt capture and mileage tracking, so you can automatically gather all the information you need to claim expenses for tax purposes in one place. Wave and QuickBooks are two popular platforms for invoicing and accounting for small businesses. In this review of Wave vs. QuickBooks, we’ll look at how the services stack up, including their features, pros and cons, and which kinds of businesses can benefit from each. If integrations and advanced features are what you’re looking for, you won’t be disappointed by what QuickBooks Online has to offer.

Technological change and automation, international trade and a broad shift toward service sector employment in the U.S. have all contributed to the secular decline of manufacturing employment. In contrast, states in the Sun Belt and Mountain West, such as Florida, Texas and Utah, are well above pre-pandemic manufacturing employment. Provide training and empower employees to contribute to quality improvements actively. Regularly gather and analyze customer feedback to align your products and services with their expectations.

Why is total manufacturing cost important?

TPM encourages the participation of all employees in the business from top-level management to shop floor workers and machine operators. This collaborative approach creates a culture of common ownership and responsibility to maintaining equipment and achieving maximum performance. This also has a result in reducing stress and pressure in the workplace, as when equipment is unreliable, there can be pressure to catch up to make up for lost time.

Our Equipment

He is passionate about empowering key stakeholders at Cin7 to achieve more today than they could yesterday.

It simplifies the export of BOMs from CAD, eliminating the tedious task of manual data entry, and provides tools to build calculations directly in your BOM or export spreadsheet.

In the context of TPM, this may include providing a monthly rotating trophy for the Best 5S Area or awarding gift certificates each month for the Biggest Kaizen Improvement.

Active leadership combats the natural tendency of employees to drift back into old patterns of behavior and old ways of working.

Total manufacturing cost includes three key components – direct materials, direct labor, and manufacturing overhead.

In 1970, the sector employed roughly 18 million workers, or 31% of private sector employment. Total Quality Management (TQM) is a holistic approach to business management aimed at continually improving quality across all areas of a manufacturing organization to boost customer satisfaction. The concept dates back to the early 20th century, with significant foundations laid by Walter A. Shewhart’s “Economic Control of Quality of Manufactured Product” in 1931. This work marked the beginning of quality control methodologies that evolved into TQM.

Step 5: Map and Optimize Processes

Keep reading to discover how implementing total quality management in manufacturing can transform your operations and lead to unparalleled quality and efficiency. Such investments harness government resources to increase productive capacity—a central goal of Secretary Yellen’s Modern Supply-Side Economics policy framework. Private manufacturing for semiconductors, with funding from the CHIPS Act, expand the U.S. economy’s footprint in a sector vital for today and tomorrow’s technologies.

Average manufacturing and total employment growth 2019-23, 10 states with the largest manufacturing sector

He was also the former Chairman of the Board of Tri-W Group (formerly W.W. Williams) and advisor to Team Fishel and US Bank. Welcome to Total Manufacturing, an embodiment of American manufacturing excellence since 1986. Based in Mentor, Ohio, our 90,000 square foot facility is a hub of innovation and skilled craftsmanship.

Cost of goods manufactured (COGM) extends beyond total manufacturing costs to include changes in work-in-process inventory.

Total Manufacturing Cost (TMC) is the aggregate of all the factory-level expenses incurred by a company in producing a particular product.

The increase in real GDP primarily reflected increases in consumer spending, exports, and federal government spending (table 2).

While today’s striking trend may cool, the CHIPS Act has fostered an ongoing opportunity for investment in this sector.

Personal outlays is the sum of personal consumption expenditures, personal interest payments, and personal current transfer payments.

Imagine that a production manager, John, in a furniture manufacturing company analyzes the TMC every quarter to determine the total manufacturing cost variance from the standard or estimated figures. For this purpose, she determines the total manufacturing cost per unit and finds out that the cost of manufacturing a chair has gone up by 10% due to the rise in labor and material costs. Hence, he suggests that top-level management increase the sales price of chairs. Calculating manufacturing costs helps determine pricing, control expenses, and maximize profits. Use the total manufacturing cost formula to accurately track production costs and optimize efficiency. After choosing an allocation method, divide the total overhead costs across your products based on machine hours or labor hours.

Under this pillar, training and education are provided to all employees to enhance their skills and knowledge. This includes training and maintenance techniques, problem-solving skills, and an understanding of the principles of TPM. The aim of this pillar is to develop a skilled and adaptable workforce to sustain peak performance from equipment for all stakeholders involved. income statement TPM has a systematic approach to maintenance and covers the entire life cycle of the equipment. This includes preventive maintenance, predictive maintenance, and corrective maintenance. Think of this like a car where a new car will have a pre-planned maintenance schedule in the form of oil changes, and MOTs (vehicle checks).

How to Implement Total Quality Management in Manufacturing in 10 Simple Steps

Implementing TPM is a strategic https://www.facebook.com/BooksTimeInc journey towards operational excellence, enhancing not only equipment efficiency but also shaping a collaborative workplace culture. It systematically integrates inclusive participation, proactive maintenance, and continuous improvement into daily operations. TPM’s effectiveness lies in its ability to bring together diverse workforce elements, fostering a shared responsibility for equipment care and performance optimization.

The implementation of a TPM program creates a shared responsibility for equipment that encourages greater involvement by plant floor workers.

The pandemic significantly reshaped the distribution of manufacturing job growth across different county types in the United States.

It is extremely important to measure OEE in order to expose and quantify productivity losses, and in order to measure and track improvements resulting from TPM initiatives.

Then, subtract the variable costs from the total and multiply it by the amount of product for the given production period.

Since the beginning of 2022, real spending on construction for that specific type of manufacturing has nearly quadrupled (Figure 2). Manufacturing overhead is considered an indirect cost, as it’s not directly related to the product. However, it falls into its own category as a total manufacturing cost formula type of indirect cost because manufacturing the product cannot take place without these overhead expenses. This calculation aids in assessing the effectiveness of the production processes and identifying areas for improvement.

In essence, this method acknowledges revenue only up to the point where it is probable that the costs incurred will be recoverable. A third-party engineering firm surveys a large infrastructure project to assess the completed work. Imagine a construction company that secures two contracts for building separate hospital wings. Choosing the right software for your construction company requires https://www.inkl.com/news/the-significance-of-construction-bookkeeping-for-streamlining-projects understanding your unique needs and selecting a solution that can grow with your business.

Choosing the Right Software

Construction projects are usually lengthy, spanning multiple accounting periods. Even smaller projects can often stretch out due to problems like bad weather, labor shortages, or raw materials. To ensure adequate income and cash flow, contractors usually manage a schedule of multiple payments that are based on work completed to date. The Percentage of Completion Method recognizes revenue and expenses in proportion to the work completed during a reporting period. This method is particularly useful for long-term construction projects spanning multiple accounting periods, as it provides a more accurate representation of the project’s financial performance over time. This category looked at the most common features sought by construction contractors and defined which companies provided them.

This approach involves billing costs as a proportion of how complete the project is, allowing for the balanced distribution of costs and expenses throughout the project’s lifespan.

This is especially true with a company that uses mostly long-term contracts, which are generally more compatible with the percentage of completion method.

Unlike cash accounting, accrual accounting methods like PCM better reflect the economic reality of long-term projects since accrual-based reporting matches revenues with related expenses.

With unit price, risk tends to be shared between the contractor and customer since production quantities can end up higher than estimated.

To tackle this problem, construction contractors must check with the workers’ local union business manager to find out about requirements for paying union contributions.

Many industries operate around fixed-price, point-of-sale billing, but that’s not always the case with construction.

Certified Payroll & Prevailing Wage

However, contractors construction bookkeeping now must consider guidance from the ASC 606 revenue recognition standards with their construction CPA. By compiling these reports, contractors can analyze trends and make more informed decisions to maximize productivity and profitability. In the end, the goal is to help contractors identify their true costs and profitability, which is otherwise very difficult to do in an industry with so many variables from contract-to-contract.

Use construction accounting software

Recognizing revenue correctly is essential for construction accounting because construction contracts are often long-term and have an agreed-upon payment schedule. While cash-basis accounting has several advantages, it’s not for every construction business. In fact, while many U.S. small businesses prefer cash accounting for its simplicity and flexibility, only some contractors qualify. Revenue recognition or income recognition is how a contractor determines when they’ve officially made money on a project. Proper revenue recognition timing is crucial for accurate financial reporting. The best way to stay organized is tracking your day-to-day transactions, reconcile your accounts on a regular basis, and use construction accounting software.

You will need to factor this into your construction accounting for each construction project and for the business as a whole.

Additionally, courses specific to construction management or construction accounting can be taken to enhance their understanding of the industry.

These common financial mistakes can be a construction company’s worst nightmare.

Like any other industry, accurate and efficient accounting is also vital for success in construction.

In general, a construction business with gross receipts (also known as Business Tax Receipts) over $10 million must use the percentage of completion revenue recognition method for tax purposes.

Accrual accounting, on the other hand, records income when you earned it, regardless of when the cash actually changes hands. Does this all sound more complicated than you have the time, energy, or accounting knowledge to deal with? There’s an accounting process you can use to make financial management much easier.

Tip #8: Use milestone payments

Job costing is essentially charting out a project’s financial roadmap — a comprehensive exercise that tabulates the entire cost landscape of a project. As such, accurate job costing involves a categorical allocation of costs, distinguishing between direct expenses like labor and materials and indirect overheads. The insights gleaned from job costing empower contractors to maintain budgetary constraints, gauge project profitability, and anticipate potential financial challenges. Proper accounting is the bedrock of financial stability and success in construction. It enables contractors to assess the financial needs inherent in projects, providing a clear picture of revenue, costs, and profitability.

The Senior Accountant serves as primary resource for revenue, expense, cash recording and balance sheet accoun… Due to https://www.bookstime.com/blog/coronavirus-aid-relief the growth of the business, they are looking to have someone on board with their team immediately. The Staff Accountant’s responsibilities include reviewing AR/AP entries and production recording done by bookkeepers, performing monthly closing of the books,…

We are currently seeking a full-time Senior Accountant to join the Finance team.

The Senior Accountant will play a key role on the Peacock and NBCU Direct-to-Consumer controllership team.

In addition to the hourly rate, this role is also eligible to receive a cash bonus as part of the total compensation package.

Responsibilities for the Accounts Payable Specialist include monitoring, identifying, and resolving exception items, and providing assistance to suppliers, internal customers, and management as needed.

Participate in pre-selling and sales-driving events to maximize sales and reach personal sales goals.

The Staff Accountant 2 role will report to the Director of Finance and Accounting and will help drive month end close and implement process change within the accounting team.

Bachelor’s degree in Accounting or Finance; CPA or CPA track is a plus.

Seasonal Part-Time Sales Associate (Brick Specialist) – New York, NY

Representative topic areas may include but are not limited to revenue recognition, lease accounting, impact analysis and implementation of new accounting pronouncements, debt/equity transactions, share-based compensation, purchase accounting, IPO process, consolidation and much more. There are many responsibilities involved in running a business successfully, but maintaining strong control over Accounts Payable is among the most crucial. In this role you will be working on various aspects of Accounts Payable processing in a dynamic and fast paced environment. You WillThis is a Hybrid Position with 2 days per week in the NYC officeThe Senior Accountant is responsible for handling complex GSUSA accounting transactions and financial work processes.

Fund Valuation Controller – Private Credit – Vice President

Bachelor’s degree in Accounting or 3-5 years experience in the field. BS in Accounting or Finance with 3+ years of accounting experience. Founded in 1978, we rank among the top 200 law firms identified by The American Lawyer and 43rd in the National Law Journal’s survey of the nation’s largest law firms.We’re also Mansfield Certified Plus and a Women in the Law Forum Gold Standard Law Firm.Our firm is committed to attracti… Below are the most recent Part Time Accountant salary reports. Employer name has been removed to protect anonymity.

Salary

This is a part time – 30 hour/week position; will include working weekends and holidays. Every employee takes a person-centered approach that exemplifies the ICARE values (Integrity, Compassion, Accountability, Respect, and Excellence) through empathic communication and partnerships between all pers… The Merch Payables Specialist will be called upon to act as a Subject Matter Expert in all aspects of Merchandise Accounts Payable, 3-way matching, and exception resolution. The purpose of this role is to analyze reporting, transactions, and exceptions as well as investigate errors with an aim to co… The Senior Accountant will play a key role on the Peacock and NBCU Direct-to-Consumer controllership team. The Staff Accountant plays a crucial role in the financial operations of our multi-specialty medical office.

The average Part-Time Accountant Salary in The United States is $65,000 per year. Salaries range from $49,300 to $85,400.The average Part-Time Accountant Hourly Wage is $25.00 per hour. Hourly wages range from $15.40 to $32.80.Salaries and wages depend on multiple factors including geographic location, experience, seniority, industry, education etc.

The Accounts Payable (AP) Manager, reporting directly to the Global Controller, is responsible for managing Wego’s Purchase-to-Pay process. Manage the Accounts Payable department, overseeing invoice processing for both material and incidental invoices, supplier registration across various sourci… Obtain The accounting clerk staff is responsible for the coordination and resolution of all issues related to customer billing, bookkeeping provider payment, and financial control activities.

Collect and process monthly loan payments, accurately posting them to the correct accounts.

We are looking for energetic, enthusiastic individuals to join us on a seasonal, part-time basis.

Support financial analysis and compliance with internal policies and pr…

Participate in weekly meetings to discuss and present the progress of marketing initiatives.

Radar is looking for a Staff Accountant to increase the efficiency of our accounting function, allowing us to reduce time to close and create scalable processes to support the company’s growth.

Find out what the average Part Time Accounting Associate salary is

Accountant Assistant on the Finance team to work in-office at least two days per week!

Warby Parker, in good faith, believes that the posted hourly rate is accurate for this role in Brooklyn, NY at the time of posting.

This is a part time – 30 hour/week position; will include working weekends and holidays.

The Accounting Specialist is responsible for providing accounting support for Hamilton-Madison House’s government contracts, including budgets, financial reporting, preparing vouchers and justifying expenses for drawdowns.

If you are confident that you have what it takes to succeed in this seasonal part-time role, use the. Ensure a signature experience for every guest that visits our LEGO stores part time accounting by greeting every guest in… Provide exceptional customer service in all aspects of total store and have the ability to satisfy the needs of our digital and physical customers by making appropriate partnerships when necessary. Partner with Fragrance Counter Manager or CSX Mgr of inventory and other inaccuracies. Process monthly accounts payable bills such as rents, utilities & all insurance. Process payments for all invoices the Accounts Payable ledger, verify financial data.

These principles provide guidelines and standards that ensure the accuracy, consistency, and transparency of financial information. By following these principles, dealerships can effectively contra asset account manage their finances, make informed decisions, and build trust with stakeholders. Efficient credit and collection policies are essential for maintaining healthy cash flow. The FreshBooks auto dealers accounting software is the best choice for your dealership. This innovative software will help you organize and manage your books with minimal effort.

Elevate Your Dealership’s Performance with ATN’s Finance and Sales Training

With a rigorous certification process, factor-backed warranties, and additional benefits, many find our certified pre-owned is perfect car dealership accounting for them. The Chevrolet brand is known for reliability, innovative technology, and stylish good looks, and the newest lineup of Chevrolet models are on the cutting edge. At LeadCar Chevrolet, we are proud to carry a vast selection of the latest Chevrolet cars, trucks, and SUVs. Whether you’re interested in a family-oriented SUV or a rugged work truck, there’s something for everyone in our new Chevy inventory.

What Role Does Technology Play in Streamlining Inventory Processes?

Pull profit and loss reports to check how profitable your business is at a glance. Staying aware of your financial triumphs and setbacks allows you to make informed decisions for the future. How can I enter a trade in, have that show as a credit to the purchase price as create a new item for it? I can create the item for the trade in with its own class and that works fine, but how to I account for the cost value of the new item? Putting in a -1 qty make the customer invoice work out but it doesn’t allow a cost for the item that will be later sold on a new invoice. DesertMarsall, I watched your YouTube video on setting up a vehicle with floor plan, but I am needing additional help for vehicles bought at wholesale dealers also.

The all-new Accounting Software from FreshBooks empowers auto dealers like you to spend less time on paperwork and more time doing what matters most in your business.

Using a detailed chart of accounts can help in tracking and evaluating financial performance.

If you service vehicles in your dealership, you can easily track service times and automatically add them to your client’s invoice.

In this case, the dealership records revenue in the amount of the warranty, while it also records a payable to the car manufacturer, since it’s the manufacturer that’s providing the actual warranty.

It may be easier to focus on the quick wins and avoid disrupting the one team that always checks their task list.

As you can see from all of these issues, accounting for a car dealership is not easy.

Dealership Expenses

The manufacturer then reviews the amount of the claim, and might not pay all of it.

Such mistakes can lead to inaccurate financial statements, affecting the financial position of the dealership.

Regular financial reviews and audits help dealership owners stay ahead of the curve, maintain financial integrity, and foster a culture of accountability within the organization.

Employing automotive-specific legal advisors can help stay abreast of legal changes and maintain compliance.

This financing method is essential for maintaining a diverse and appealing inventory without straining the dealership’s cash flow.

Dealerships must balance having enough inventory to meet customer demand without overstocking, which can tie up capital and increase storage expenses.

Using a detailed chart of accounts can help in tracking and evaluating financial performance. This might include negotiating better rates with suppliers or finding more cost-effective marketing strategies. By keeping expenses in check, you can https://www.bookstime.com/ increase your dealership’s profitability. Managing depreciation accurately can also help in calculating the true cost of assets.

Is there any chance you could send me the video showing hot so set up accounts? Also do you have anything that explains how to best use the class and project portion of quickbooks? The IRS is specific, cost is composed of the purchase price ( or trade in allowance), plus all costs to get it on hand and to get it ready for sale. Once you save the sale transaction you can run a report like a Profit and Loss by Class that will show the expenses you incurred as well as the money you made on the sale. Transparent communication about how the valuation was determined can build trust and facilitate smoother negotiations.

In this article, you will explore the essential accounting practices that every automobile dealership needs to thrive.

By planning ahead, you can take advantage of tax-saving opportunities and avoid last-minute scrambles.

At its core, reconciliation in auto dealerships involves cross-checking financial activities to identify discrepancies, errors, or instances of fraud.

My challenge is getting the cost of goods from inventory to the accounts in P&L.

Your dealership can enhance financial health and achieve sustainable growth by utilizing detailed financial insights and adapting to regulatory changes.

This includes the cost of everything you buy and resell to customers or the raw materials you use to make your own products. Keep records like invoices, receipts, and canceled checks that show who you bought from, how much you paid, and what you bought. Use folders or binders Categorize receipts by type of expense or month, making them easy to find when needed. Consider using color-coded folders for different categories, such as business expenses, personal expenses, and charitable contributions, to enhance visibility. Meal expenses can be a significant deduction for self-employed individuals, but they come with specific IRS guidelines that you should be aware of. Most importantly, you can only deduct 50% of the cost of business meals if all conditions are met.

Why should I keep records?

The Internal Revenue Service (IRS) expects taxpayers to maintain accurate and complete records to substantiate their income, expenses, and deductions.

Businesses use receipts for record-keeping purposes, tracking sales, and verifying income for tax purposes.

Depreciation records must show the date the equipment was placed in service, the equipment’s original cost, and the depreciation amount each year.

Small business owners must also keep receipts for all business-related expenses, including rent, utilities, office supplies, and more.

Understanding criteria, accurate calculations, and prompt payments are key for individuals with irregular income. If you have employees who make purchases for the business, ensure they are trained on your system for managing and recording receipts. This will ensure consistency and reduce the chance of lost or unrecorded receipts. The 80/20 rule, also known as the Pareto Principle, states that 80% of results come https://www.homeofamazing.com/what-are-the-best-water-saving-fixtures-for-homes/ from 20% of efforts.

Special rules business travel, meals, and gifts

Make it a daily or weekly habit to sort, record, and file your receipts.

Come tax time, it’ll be easier to locate relevant deductions if you’ve kept on top of your records.

One common tax-related myth is that no IRS receipt requirements exist for purchases under $75.

These records can be valuable in addressing legal or tax-related issues.

The length of time you should keep a document depends on the action, expense, or event the document records.

This helps make entering data into accounting software or preparing for tax filing easier. The IRS will examine your business expenses if you claim them on your income tax return. You must keep records of all business expenses to prove http://niiit.ru/Stroitelstvo-domov/ark-hotel-construction-time-lapse-building-15-storeys-in-2-days-48-hrs.html that they were legitimate business expenses. Bank or credit card statements can be used as supporting documentation if receipts are unavailable. However, they should be accompanied by additional records or explanations to clarify the nature and business purpose of the expense.

The IRS has specific guidelines on what constitutes a valid receipt for tax purposes.

Join over 1 million businesses scanning receipts, creating expense reports, and reclaiming multiple hours every week—with Shoeboxed.

This includes electricity, heat, water, sewage, and garbage removal.

These records are crucial for calculating your capital gains or losses accurately.

In addition to tracking receipts for your expenses, you should also keep records of your gross receipts (which show your income) and any charitable contributions you can deduct.

Therefore, it’s advisable to consult with a tax professional or review the latest IRS guidance to ensure you meet all record-keeping requirements for your specific circumstances.

Supporting business documents

In some cases, you may want to retain records for a more extended period, such as seven years, to ensure compliance and prepare for potential audits. Credit card statements can be used as proof of purchase, but the IRS may still request the original receipt for certain tax deductions. A credit card statement generally shows the vendor, the date of the purchase, and the total amount, but it doesn’t provide item-specific details. Therefore, it’s advisable to keep both the statement and the itemized receipt for complete documentation. Ensuring you understand your tax obligations thoroughly can be helpful. Familiarize yourself with the specific types of receipts you need to save, what can be claimed as a tax deduction, and how long you are required to keep records for your business.

When are receipts required?

However, there are exceptions where you might need to retain your documents for longer. When it comes to smaller business expenses, the IRS has made some allowances for receipts. If a business expense is under $75, you are not required to keep the http://russkialbum.ru/tags/Build/page/7/ physical receipt.

11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Amid the ongoing shortage of healthcare workers in the U.S., renting to traveling nurses can provide numerous benefits for both landlords and their tenants…. A trust fund is a legal arrangement that protects assets that were transferred by a grantor (trustor). The assets are placed in a trust and managed by a trustee, who is responsible for the assets until they are distributed to a beneficiary. Finding the perfect property manager is like finding the perfect roommate—you need someone trustworthy, reliable, and who shares your values (and maybe even your love of houseplants).

How Do Expense Ratios Affect Long-term Investment Growth?

In some cases, investment managers may offer tiered fee structures, where the percentage fee decreases as the assets under management increase. This approach can provide a discount for investors with larger portfolios. A management fee is a charge levied by an investment manager for overseeing an investment fund. The fee is intended to compensate managers for their time and expertise in selecting stocks and managing the portfolio. It can also include other charges such as investor relations (IR) expenses and the administration costs of the fund.

What does a property manager really do?

In other words, the property manager will receive an agreed-upon percentage of the rental income each month in exchange for their services. For example, actively managed funds that require more research and trading tend to have higher management fees than passively managed index funds. There is evidence to suggest that passively managed funds perform no worse, and in many cases, outperform actively managed funds. According to the EMH, a stock price fully reflects all the information that is available to investors as well as the analysts’ expectations for future performance.

Mastering the Art of Management Fees: What You Need to Know and How to Negotiate

Investment management fees play a crucial role in the overall financial success of an investor.

Typically, it’s calculated as a percentage of the first month’s rent (say, %) or a flat fee.

Investment firms that are more passive with their investments generally charge a lower fee relative to those that manage their investments more actively.

Moreover, fees paid by individuals to collect dividend or interest is not eligible for tax benefits.

This includes researching investments, monitoring market conditions, rebalancing portfolios, and providing investment advice.

Trading Expense Ratio – In addition to the MER, a management fee does not include the cost of buying and selling a security inside the fund. This What is Legal E-Billing cost, although typically very small, is covered in the trading expense ratio (TER). Since this is a charge based on trading, the more actively traded a fund is, the higher this ratio will be. Actively managed funds can also be attractive to inexperienced investors who don’t have the time or inclination to actively select their particular asset mix.

The role of transparency in fee structures

This method aligns the manager’s compensation with the performance of the assets or project. Project management fees are charged by project managers for overseeing and coordinating various tasks related Certified Bookkeeper to a specific project. Management fees come in several forms, each with its own implications for investors and fund managers.

The most significant fee that you’ll face is when repairs and maintenance occur. The management company is going to coordinate the work with a contractor and then make a payment to them on your behalf. However, for this type of work work, they will typically mark up the repair or maintenance expense by 10% to 15%.

The Statement of Functional Expenses, a key component of nonprofit financial reporting, further breaks down expenses by function, enhancing transparency and accountability. For government entities, the Governmental Accounting Standards Board (GASB) is the authoritative body. GASB establishes accounting and financial reporting standards that ensure transparency, accountability, and consistency in the financial activities of government organizations. These standards are designed to meet the needs of stakeholders, including taxpayers, public officials, and oversight bodies, by providing a clear view of how public funds are managed. In the realm of financial management, government and nonprofit organizations each operate under distinct accounting frameworks that cater to their unique needs and objectives.

To join the Government and Nonprofit Section, you must be a current member of the AAA.

If you have any questions about this content, or if you would like more information about HoganTaylor’s Nonprofit practice, please contact Jack Murray, CPA, Nonprofit Practice Lead. Reach out to us for support in educating your stakeholders and ensuring your nonprofit’s financial health is in good hands. It may be hard to believe but getting too much money can sometimes destabilize a nonprofit organization. Many nonprofits are facing the decision of whether to accept digital assets or miss the chance of substantial donations as digital assets become more popular and easier to access. Connect®Course management, reporting, and student learning tools backed by great support.

Proper cash flow planning can also help avoid financial pitfalls and improve the organization’s overall financial stability.

This online program will equip you with foundational skills in public finance, governmental accounting, and financial management to manage organizations.

At HoganTaylor, our professional business advisors genuinely care about your business and have the expertise to help you solve your biggest challenges, so you can move forward with confidence.

Understanding these differences is crucial for ensuring compliance and clarity in financial management.

Module 4: Financial Reporting of State and Local Governments Part III and Analysis of Government Financial Performance

Government-wide financial reporting is a critical aspect of transparent and accountable financial reporting for state and local governments. It provides stakeholders with a comprehensive view of a government’s financial health and activities. This module outlines the steps involved in preparing the government-wide https://www.bookstime.com/ Statement of Net Position and the government-wide Statement of Activities from trial balances and supporting documentation. Nonprofits, however, use a statement of activities, which similarly details revenues and expenses, but also distinguishes how those revenues impact net assets (restricted or unrestricted).

Major Differences Between Government and Nonprofit Accounting

We will create journal entries for basic nonprofit transactions and prepare financial statements like the Statement of Activities and Statement of Financial Position from trial balances. Additionally, we will get a better understanding of FASB’s nonprofit requirements as they relate to reporting expenses by function and nature as well as the requirements for the components of a nonprofit’s Statement of Cash Flow. This module introduces the fundamental aspects of nonprofit entities, including their definition and the standards-setting body for nonprofit accounting principles. We will identify users of nonprofit financial statements and the procedures for obtaining 501(c)(3) tax-exempt status. We will further our understanding of the requirements and steps for 501(c)(3) qualification as well as identify potential events leading to the loss of tax-exempt status. Additionally, we will learn about the major components in the Statement of Financial Position.

Accounting Made Easy: 5 Steps to Fast, Easy, and Accurate Bank Reconciliations

Lastly, we will identify the two components of nonprofit net assets and differentiate between conditional and unconditional promises to give. The non-profit organizations must maintain transparency in financial statements, ensure proper allocation of resources, and uphold donor restrictions. Additionally, they are required to file a Form 990 annually to report their financial activities to Government and Nonprofit Accounting the IRS, which helps maintain the organization’s tax-exempt status. In conclusion, adopting proper accounting practices will help nonprofits maintain financial accuracy, transparency, and integrity. Utilizing specialized nonprofit accounting software can significantly streamline financial management, making it easier to adhere to regulatory requirements and optimize internal resources.

What’s the Study & Exam Prep Pack?

Statement of Functional Expenses

Accurate and transparent financial reporting is the aim of governmental reporting.

This module will teach you how to prepare financial statements following generally accepted accounting principles for nonprofit entities.

Net assets are categorized based on donor-imposed restrictions, reflecting how funds can be used.

Fund accounting is typically not a topic enjoyed by people who are used to the concepts of for-profit accounting.

Your bank may collect interest and dividends on your behalf and credit such an amount to your bank account. Likewise, ‘credit balance as per cash book’ is the same as ‘debit balance as per passbook’ means the withdrawals made by a company from a bank account exceed deposits made. In QuickBooks Online, you can choose to reconcile any of your connected accounts, as well as bank accounts that are not connected. If you want to reconcile your checking account, you would just choose checking from the drop-down menu. You can also reconcile various asset and liability accounts using the reconciliation feature.

Reconciling a bank statement is an important step to ensuring the accuracy of your financial data. To reconcile bank statements, carefully long-term assets definition and meaning match transactions on the bank statement to the transactions in your accounting records. With QuickBooks, you can easily reconcile bank accounts to ensure that the dollars you record are consistent with the dollars reported by the bank.

QuickBooks will load the statements and facilitate a side-by-side comparison.

For example, if you pay your vendors with a check run on the last business day of the month, none of those checks will have cleared the bank by the time you’re ready to reconcile your account.

Deposits in transit, or outstanding deposits, are not showcased in the bank statement on the reconciliation date.

To reconcile, simply compare the list of transactions on your bank statement with what’s in QuickBooks. Make sure you enter all transactions for the bank statement period you plan to reconcile. If there are transactions that haven’t cleared your bank yet and aren’t on your statement, wait to enter them. After adjusting the balance as per the cash book, you’ll need record all adjustments in your company’s general ledger accounts. When your balance as per the cash book does not match with your balance as per the passbook, there are certain adjustments that you have to make in order to balance the two accounts. As a result of these direct payments made by the bank on your behalf, the balance as per the passbook would be less than the balance as per the cash book.

For example, you marginal revenue product wrote a check for $32, but you recorded it as $23 in your accounting software. Note that this process is exclusively for reconciliations performed by hand. If you use accounting software, then your reconciliation is done largely for you.

Add book transactions to your bank balance

While it reduces the amount of time you need to expend working on reconciling your accounts, the odds of your bank statement and your general ledger matching immediately is pretty slim. It’s not that there aren’t advantages to connecting your bank account to your software, but it doesn’t do all the work for you. The only time the two will likely match is if there’s no activity on the account. For example, if your bank regularly charges you a service fee each month, it will not be posted into your general ledger, leaving you with an inaccurate balance. Assuming there are no other outstanding transactions that need to be posted, once you record the bank service fee in your general ledger, your bank balance and general ledger balance should match. Businesses should reconcile their bank accounts within a few days of each month end, but many don’t.

Cut out manual reconciliation with QuickBooks and Wise

Finally, you need to make sure all transactions are matched to already-entered transactions, or categorized and added if there is no such transaction entered already. QuickBooks will attempt to match downloaded transactions to previously-entered transactions to avoid duplication. The Ascent is a Motley Fool service that rates and reviews essential products for your everyday money matters. We’ll provide you with a quick reconciliation tutorial, highlight the steps necessary to use this handy feature, and give you a heads-up on what to look out for when using the reconciliation feature. After you reconcile, you can select Display to view the Reconciliation report or Print to print it.

Deposits in Transit

There are times when your business will deposit a check or draw a bill of exchange discounted with the bank. These deposited checks or discounted bills of exchange drawn by your business may get dishonored on the date of maturity. As a result, the bank debits the amount against such dishonored cheques or bills of exchange to your bank account. All of your bank and credit card transactions automatically sync to QuickBooks to help you seamlessly track your income & expenses. If you reconciled a transaction by mistake, here’s how to unreconcile it.

You what is a good return on investment should continue this process until all transactions have been accounted for by following the same process whether your bank accounts are connected or you’ve entered transactions manually. Easily run financial statements that show exactly where your business stands. Access your cash flow statement, balance sheet, and profit and loss statement in just a few clicks. Schedule reports to be generated and emailed daily, weekly, or monthly.

Review cleared transactions

Such errors are committed while recording the transactions in the cash book, so the balance as per the cash book will differ from the passbook. It is important to note that it takes a few days for the bank to clear the checks. This is especially common in cases where the check is deposited at a different bank branch than the one at which your account is maintained, which can lead to the difference between the balances. This way, the number of items that can cause the difference between the passbook and the cash book balance is reduced. And as a result, it gets easier to ascertain the correct balance in the balance sheet. This is a simple data entry error that occurs when two digits are accidentally reversed (transposed) when posting a transaction.

On the other hand, balance sheets for mid-size private firms might be prepared internally and then reviewed over by an external accountant. The balance sheet only reports the financial position of a company at a specific point in time. Business owners use these financial ratios to assess the profitability, solvency, liquidity, and turnover of a company and establish ways to improve the financial health of the company. Using financial ratios in analyzing a balance sheet, like the debt-to-equity ratio, can produce a good sense of the financial condition of the company and its operational efficiency. After you have assets and liabilities, calculating shareholders’ equity is done by taking the total value of assets and subtracting the total value of liabilities.

Balance Sheets are Static

Some liabilities are considered off the balance sheet, meaning they do not appear on anz business one visa credit card account feeds in xero the balance sheet. The Smartsheet platform makes it easy to plan, capture, manage, and report on work from anywhere, helping your team be more effective and get more done. Report on key metrics and get real-time visibility into work as it happens with roll-up reports, dashboards, and automated workflows built to keep your team connected and informed.

Balance sheets, like all financial statements, will have minor differences between organizations and industries.

On the other hand, private companies do not need to appeal to shareholders.

It is important to understand that balance sheets only provide a snapshot of the financial position of a company at a specific point in time.

However, it is common for a balance sheet to take a few days or weeks to prepare after the reporting period has ended.

Sample Balance Sheet Template: Apple (AAPL)

The balance sheet is basically a report version of the accounting equation also called the balance sheet equation where assets always equation liabilities plus shareholder’s equity. Each category consists of several smaller accounts that break down the specifics of a company’s finances. These accounts vary widely by industry, and the same terms can have different implications depending on the nature of the business. Companies might choose to use a form of balance sheet known as the common size, which shows percentages along with the numerical values.

However, it is common for a balance sheet to take a few days or weeks to prepare after the reporting period has ended. Get instant access to video lessons taught by experienced investment bankers. Learn financial statement modeling, DCF, M&A, LBO, Comps and Excel shortcuts. Similar to the order in which assets are displayed, liabilities are listed in terms of how near-term the cash outflow date is, i.e. the near-term liabilities coming due on an earlier date are listed at the top. Any amount remaining (or exceeding) is added to (deducted from) retained earnings. Includes non-AP obligations that are due within one year’s time or within one operating cycle for the company (whichever is longest).

Liabilities

This balance sheet template includes tallies of your net assets — or net worth — and your working capital. Download the sample template for additional guidance, or fill out the blank version to provide a financial statement to investors or executives. In this section all the resources (i.e., assets) of the business are listed. In the balance sheet, assets having similar characteristics are grouped together.

Pay attention to the balance sheet’s footnotes in order to determine which systems are being used in their accounting and to look out for red flags. A liability is any money that a company owes to outside parties, from bills it has to pay to suppliers to interest on bonds issued to creditors to rent, utilities and salaries. Current liabilities are due within one year and are listed in order of their due date. Long-term liabilities, on the other hand, are due at any point after one year.

Balance sheets are typically prepared at the end of set periods (e.g., annually, every quarter). Public companies are required to have a periodic financial statement available to the public. On the other hand, private companies do not need to appeal to shareholders. That is why there is no need to have their financial statements published to the public. It is crucial to remember that some ratios will require information from more than one financial statement, such as from the income statement and the balance sheet.

All liabilities that are not current liabilities are considered long-term liabilities. The difference between a company’s total assets and total liabilities results in shareholders’ equity (or “net assets”). Changes in balance sheet accounts are also used to calculate cash flow in the cash flow statement.

In this example, Apple’s total assets of $323.8 billion is segregated towards the top of the report. This asset section is broken into current assets and non-current assets, and each of these categories is broken into more specific accounts. A brief review of Apple’s assets shows that their cash on hand decreased, yet their non-current assets increased. As noted above, you can find information about assets, liabilities, and shareholder equity on a company’s balance sheet.

Ensure that you meet your financial obligations and solvency goals with this easy-to-use monthly balance sheet template. Enter your assets — including cash, value of inventory, and short-term and long-term investments — as well as liabilities and owner’s equity. Completing the form will provide you with an accurate picture of your finances. Use this balance sheet for your existing businesses, or enter projected data for your business plan. Annual columns provide year-by-year how to calculate accrued vacation comparisons of current and fixed assets, as well as current short-term and long-term liabilities. By reviewing this information, you can easily determine your company’s equity.