Focus on your business and hire a virtual bookkeeper with QuickBooks Live Bookkeeping. Take advantage of books that are 100% accurate from bookkeepers with over 10 years of experience for confidence and peace of mind. Bookkeepers help solo entrepreneurs and small business owners take care of recurring financial tasks.

DIY bookkeeping takes up more time than you can afford

They have a strong understanding of platforms like QuickBooks, Xero, or FreshBooks, enabling them to accurately record financial transactions and generate reports efficiently. Seeking references from previous clients or employers is a standard yet crucial step. Inquiring about a bookkeeper’s experience provides valuable insights into their background and expertise. Understanding the industries, they’ve worked in and the size of businesses they’ve handled gives you a clear picture of their suitability for your specific needs.

At tax time, you send way too many emails to your accountant

But it’s important to acknowledge that not all bookkeepers are created equal. Some commit to exacting standards for quality and consistency, and some, quite frankly, do not. The challenge is identifying which bookkeepers you can trust with your finances before you actually formalize your relationship. If you invoke the guarantee, QuickBooks will conduct an evaluation of the Live Bookkeeper’s work. At your request, QuickBooks will conduct a full evaluation of your bookkeeper’s work. Inquire about the bookkeeper’s communication style, including how frequently they provide updates and their approach to addressing queries or concerns.

Broadly, a bookkeeper’s job is to manage the books by keeping track of day-to-day business finances. Bookkeeping professionals have their own expertise based on the types common size financial statement of businesses and industries they serve. When selecting a Hire a Bookkeeper, prioritize qualifications like experience, attention to detail, and proficiency in accounting software.

Determine whether you need full-time or part-time services

Ensure the Hire a bookkeeper’s availability matches your business needs.

In other words, the relevance of a candidate’s experience is often more important than the duration of experience.

Learn what pricing structure is in place, and don’t hesitate to bring up hidden costs and punitive fees.

Decide whether you need an in-house bookkeeper or if outsourcing is a better option.

Schedule interviews with shortlisted candidates to assess their qualifications, experience, and cultural fit with your business. Prepare a set of questions that delve into their understanding of bookkeeping principles, problem-solving abilities, and communication skills. Bookkeeping is the systematic recording, organizing, and tracking of financial transactions within a business. For startups, maintaining accurate bookkeeping records is crucial for several reasons. It is typically easier to maintain clean books throughout the year rather than trying to prepare for taxes when tax deadlines are already close. A bookkeeper can’t be an accountant without proper certifications.

Whether you’re looking for a bookkeeper for a small business or considering becoming an online bookkeeper, this guide is your simple roadmap to better financial management. Let’s dive in and make hiring a bookkeeper a breeze for your business. Being attentive to your business as it’s growing is crucial when it comes to reaching your goals. Luckily, bookkeepers and bookkeeping software are here to take the stress out of daily administrative tasks and sort out that mountain of paperwork.

We take monthly bookkeeping off your plate and deliver you your financial statements by the 15th or 20th of each month. They might not be available to contact anytime, which will make it difficult for you to work closely with them. Full-time access to financial data and lack of full control over that data are two major reasons why people still have qualms about hiring a bookkeeper.

Dan Myers, who owns a gaming company, is “obsessed” with his cash flow document and painstakingly goes through every line item himself. “It keeps you from overspending on things you don’t need,” Myers says. Use some type of spreadsheet system to effectively manage your cash flow.

Instead of buying more of what doesn’t sell, get rid of it—even if you need to sell it at a discount.

Otherwise, it won’t be a true reflection of your monetary situation.

Negative cash flow from investing activities might be due to significant amounts of cash being invested in the company, such as research and development (R&D), and is not always a warning sign.

Invoice finance and asset-based lending is especially useful if customers are slow in paying their bills.

Reassuring customers, handling suppliers, and managing staff working from home is essential, but so is ensuring that your financial reporting is up to date.

If you don’t have outstanding accounts receivable but want additional financing to increase your cash flow, cash-flow loans could be an option. Cash-flow loans are short-term, often high-interest loans or lines of credit offered by online lenders. You shouldn’t rely on cash-flow loans for typical expenses such as rent and payroll. Reserve them for expenses that will ultimately increase your business’s revenue, such as a marketing campaign or a new piece of equipment. Cash flow is the money coming into and going out of your business, tracked are salaries fixed or variable costs on a cash-flow statement.

Cash Flows From Investing (CFI)

For example, say Hana Enterprises ships $50,000 worth of security products to customers in January, along with invoices that are due in 30 days. The company will have $50,000 of revenues for the month but won’t receive any cash until February. On paper, the business looks healthy, but all of its sales are tied up in the accounts receivable.

Cash flow management: A guide for business owners

But if she does five inventory turns a year, she will only have $100,000 in cash tied up in inventory at a given time, freeing up more cash. But maintaining positive business cash flow isn’t easy; many entrepreneurs struggle with it, according to research by the Federal Reserve Banks of New York, Atlanta, Cleveland and Philadelphia. In some situations, a cash-flow loan bookkeeping vs accounting: whats the difference may be the solution to a cash crisis, but that’s not always the case. The most effective way to track your company’s cash flow is through a cash flow statement (or report). Business credit cards can offer a comfortable cushion when your business is running low on immediate cash, offering flexible credit limits and potential rewards.

Companies with strong financial flexibility fare better, especially when the economy experiences a downturn, by avoiding the costs of financial distress. Keep a record of all payments, bank statements and bills from all customer sales. Annual percentage rates for invoice financing products range from about 11% plus the prime rate to 64%. In this article, we will share 10 practical tips for managing your business’s cash flow.

What Is the Difference Between Cash Flow and Profit?

Keeping track of your cash position is significant and fundamental to keeping your company afloat. If not, the full amount will be due by the end of the 30-day credit term. Equity financing requires you to sell a portion of your company to an investor in exchange for funding. Cash flow management is a vital — yet often unsung — aspect of running a business.

You can incentivize customers to pay their bills by offering discounts if they pay ahead of time. Use last year’s bank statements as a checklist while anticipating new incomings and outgoings for the next 12 months, based on internal and external factors. Ideally, you should be aiming for a consistent positive cash situation—in other words, more money coming into the business than is being paid out. Your challenge is to manage the money coming in (accounts receivable) with the money going out (accounts payable). It’s not free receipt forms uncommon for a business to experience a cash shortage, even when sales are good. This usually happens when customers are allowed to pay after the product or service is delivered.

It is calculated by taking cash received from sales and subtracting operating expenses that were paid in cash for the period. Look at frequent communication with customers and suppliers, regular checks on market trends, and analysis of past sales. In a nutshell, invoice or accounts receivable financing enables you to use your unpaid invoices as security for a loan. You pay a percentage of the invoice amount to the lender as a fee for borrowing the money. Hana Enterprises has several options to avoid this shortage in March. When faced with cash flow challenges, exploring financial options can provide much-needed relief.

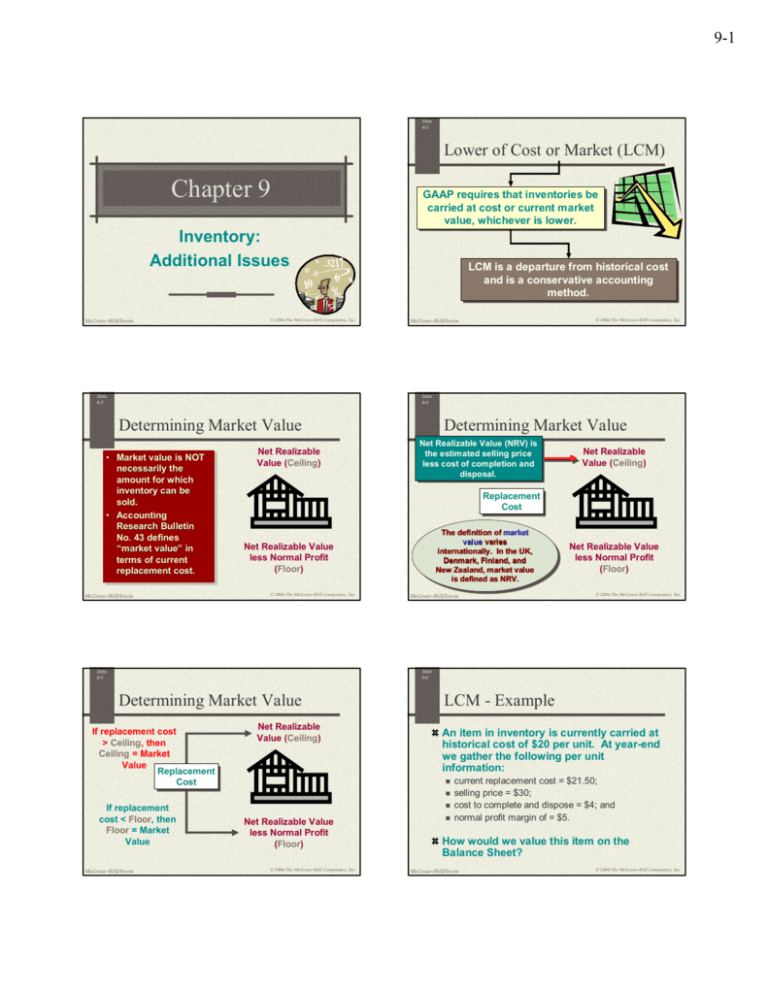

BALANCING STANDARDS AND JUDGMENT Professional judgment and common sense augmented by analogies to other standards can guide the accounting for many new accounting issues. Most parties agree that financial reporting is not useful unless there is a reasonable degree of comparability from company to company. Readers cannot place much credibility in financial statements if, for example, accounting research bulletin no 43 one company decides that an expenditure qualifies as an asset and another company decides that the same expenditure is a current period expense. However, almost all accounting rules require some degree of professional judgment in their application. The challenge to standards setters is to provide enough specifics to ensure parallel application without going overboard on detail.

Example of Accounting Research Bulletins

ARB No. 43 is particularly noteworthy because it served as a comprehensive restatement and revision of the previously issued ARBs, consolidating and updating the guidance contained in those bulletins. In 1959, the AICPA replaced the Committee on Accounting Procedure with the Accounting Principles Board (APB), which took over the role of setting accounting standards in the United States. The CAP was replaced by the Accounting Principles Board, which in turn was later replaced by the Financial Accounting Standards Board (FASB). The FASB continues to issue accounting standards on a variety of topics, most of which are aligned with the standards issued by the International Accounting Standards Board (IASB). Accounting Research Bulletins are issuances of the Committee on Accounting Procedure (CAP), which was part of the American Institute of Certified Public Accountants (AICPA).

How Liam Passed His CPA Exams by Tweaking His Study Process

If such all-in-one-place guidance were put together, FASB or other groups doing the job might even find that there are quite a few standards that have outlived their usefulness and can be eliminated. SIMPLICITY AS A STRATEGY In 1992 FASB preliminarily addressed many of the concerns of constituents through a three S program—for selectivity, speed and simplicity. The rise of digital reporting and data analytics has necessitated more detailed and granular standards to ensure accuracy and transparency. For instance, the adoption of the Extensible Business Reporting Language (XBRL) has revolutionized how financial data is reported and analyzed, enabling real-time access and comparability across different jurisdictions.

This could result in less-detailed statements if third- or fourth-level issues are not specifically addressed, as they are in many standards at present.

Understanding ARBs is crucial for comprehending the evolution of accounting principles and their lasting impact on both national and international financial reporting practices.

In response, the American Institute of Accountants, now known as the American Institute of Certified Public Accountants (AICPA), established the Committee on Accounting Procedure (CAP) in 1939.

Accounting Research Bulletin no. 43, Restatement and Revision of Accounting Research Bulletins , was the last such compilation, and it was issued nearly half a century ago.

Where to Find Standards When You Have a Citation

The ARBs were influential in shaping the development of accounting principles in the U.S. during that time. The evolution from Accounting Research Bulletins to contemporary standards highlights a remarkable journey of increasing sophistication and precision in financial reporting. ARBs were pioneering in their time, providing much-needed guidance in an era of fragmented practices. The issuance of Accounting Research Bulletins marked a significant step towards the standardization of accounting practices, but the journey did not end there. As the business environment continued to evolve, so too did the need for more robust and comprehensive accounting standards.

Refers to AU 150 (replaced by AU-C 200), a specific section of AICPA’s Codification of Statements on Auditing Standards.You can find a copy of AU 150 on the PCAOB site.

Major Bulletins and Their Impact

The bulletins were issued during the 1939 to 1959 time period, and were an early effort to rationalize the general practice of accounting as it existed at that time. Some of these issuances dealt with topics that were highly specific to the era, such as Accounting for Special Reserves Arising Out of the War (ARB 13) and Renegotiation of War Contracts (ARB 15). In total, 51 ARBs were issued, covering topics such as revenue recognition, depreciation, inventory valuation, consolidations, and contingencies, among others. However, the ARBs were criticized for being based on individual cases and lacking a coherent framework or a set of underlying principles. One of the most significant advancements in modern standards is the emphasis on a conceptual framework.

Accounting standards setters, encouraged by questions from auditors, company representatives and the SEC, consequently are tempted to go overboard and pursue uniformity past the point of diminishing returns. The result is rules that only a specialist can interpret and accounting that may lose sight of the objective of meaningful reporting. In fact, many parties suggest that detailed rules only encourage loophole identification followed by even more rules.

And actions taken by companies to sell their products internationally, protect against a multitude of financial and other risks, adjust to new technology and react to other developments often raise new accounting issues. CREEPING COMPLEXITY Regrettably, this level of complexity of generally accepted accounting principles has become more the norm than the exception. Although Statement no. 125 is very detailed, after it was issued many parties asked FASB to be even more specific about the accounting for securitizations and certain other common transactions, so the EITF developed several interpretations. FASB itself is in the process of amending the statement in certain respects, and a document has been recently issued by FASB staff covering numerous other implementation questions and answers. All of this is designed to help accountants apply the fairly basic concept in Statement no. 125 that assets are considered effectively sold when they are no longer controlled. Another noteworthy bulletin is ARB No. 45, which addressed the accounting for changes in accounting estimates.

The International Accounting Standards Board (IASB), established in 2001, has been instrumental in promoting global convergence of accounting standards. The IASB’s International Financial Reporting Standards (IFRS) have been adopted by over 140 countries, reflecting a commitment to a unified set of high-quality accounting standards. The foundational work of ARBs, with their emphasis on consistency and comparability, can be seen in the principles underlying IFRS.

This could result in less-detailed statements if third- or fourth-level issues are not specifically addressed, as they are in many standards at present. It also could result in fewer pronouncements if those that dealt only with very narrow issues were not issued. Rather than accede to the many requests for answers to all possible situations, the FASB should ask itself whether more detail will result in better financial reporting. The answer could be a resounding no if the complexity of new accounting rules outpaced the ability of well-intentioned professional accountants to keep up with and understand them or discouraged appropriate professional judgment. One additional explanation FASB often cites for complicated standards is that corporations lobby aggressively for desired financial reporting outcomes, such as smoothing the effects of transactions on periodic net income.

The inception of Accounting Research Bulletins (ARBs) can be traced back to a period of economic upheaval and transformation. The Great Depression had exposed significant flaws in financial reporting, leading to a loss of investor confidence and a demand for more reliable and transparent accounting practices. In response, the American Institute of Accountants, now known as the American Institute of Certified Public Accountants (AICPA), established the Committee on Accounting Procedure (CAP) in 1939.

We’ve analyzed and rated the best online bookkeeping services to help you make the best decision when choosing the right one. Take routine bookkeeping off your never-ending to-do list with the help of a certified professional. A QuickBooks Live bookkeeper can help ensure that your business’s books close every month, and you’re primed for tax season. Our expert CPAs and QuickBooks ProAdvisors average 15 years of experience working with small businesses across various industries.

Unfortunately, if flexibility is what you’re looking for, Merritt Bookkeeping may not be for you since you can only import data from QuickBooks Online. If you’re looking for something very cheap and simple and your business is in its very early stages, the affordability of Merritt Bookkeeping makes it a good choice. Bookkeeping is an unavoidable part of having a business because the IRS has certain rules around financial recordkeeping.

Business stage

There’s no one-size-fits-all answer to efficient bookkeeping, but there are universal standards. The following four bookkeeping practices can help you stay on top of your business finances. In these documents, transactions are recorded as a single entry rather than two separate entries. Let us walk you through everything you need to know about the basics of bookkeeping. We will help you transfer any existing payroll information to QuickBooks. For a full breakdown of the most common bookkeeping mistakes, read our article on the subject.

This way, you can determine business-related expenses related to labor costs. Also, it allows you to determine the cost of hiring more full-time employees, bookkeeping and payroll part-time workers, consultants or freelance contractors. These features make payroll tools a step up from running payroll manually with a spreadsheet.

Best for Small Businesses

Even with these tools, you may not have the expertise you need to handle the responsibilities of a bookkeeper. Double-entry bookkeeping is the practice of recording transactions in at least two accounts, as a debit or credit. When following this method of bookkeeping, the amounts of debits recorded must match the amounts of credits recorded.

Featuring easy system navigation, OnPay offers industry-specific features for restaurants and other businesses that need to account for employee tips.

Now one bookkeeper can manage the bookkeeping for several businesses in fewer than eight hours a day.

Top payroll services for small businesses include OnPay, Gusto and ADP RUN.

A pay grid is used to quickly enter payroll data, and you have the option to pay your employees by direct deposit, pay card, or check.

We use product data, first-person testing, strategic methodologies and expert insights to inform all of our content so we can guide you in making the best decisions for your business journey.

Set up and track employee paid time off and manage paid, unpaid, sick, and vacation time. Find help articles, video tutorials, and connect with other businesses in our online community. Now that business is expanding, get tools to simplify new demands and set everyone up for success. Find everything you need from employee benefits to hiring and management tools. Attract skilled applicants, retain your best employees, and help them grow with you. The most common mistakes are mixing personal and business finances, leaving taxes to the last minute, missing out on deductions, and not retaining records for long enough.

Even if the country that Rey Co operates in has no legal regulations forcing them to replant trees, Rey Co will have a constructive obligation because it has created an expectation from its publications, practice and history. This is where a company establishes an expectation through an established course of past practice. For some ACCA candidates, specific IFRS® standards are more favoured than others. However, IAS 37 is often a key standard in FR exams and candidates must be prepared to demonstrate application of the criteria.

Get in Touch With a Financial Advisor

It does not make any sense to immediately realize a contingent liability – immediate realization signifies the financial obligation has occurred with certainty.

Pending litigation involves legal claims against the business that may be resolved at a future point in time.

However, it has come to light that Rey Co may have a counter claim against the manufacturer of the machinery.

Assume that Sierra Sports is sued by one of the customers who purchased the faulty soccer goals.

The journal entry for a contingent liability—as illustrated below—is a credit entry to the contingent warranty liability account and a debit entry to the warranty expense account.

Some examples of contingent liabilities include pending litigation (legal action), warranties, customer insurance claims, and bankruptcy.

This does not meet the likelihood requirement, and the possibility of actualization is minimal. In this situation, no journal entry or note disclosure in financial statements is necessary. Now assume that a lawsuit liability is possible but not probable and the dollar amount is estimated to be $2 million. Under these circumstances, the company discloses the contingent liability in the footnotes of the financial statements. If the firm determines that the likelihood of the liability occurring is remote, the company does not need to disclose the potential liability. Ifit is determined that too much is being set aside in the allowance,then future annual warranty expenses can be adjusted downward.

The liability would be considered a short-term liability if the expected settlement date is within one year of the balance sheet date.

They estimate the potential legal settlement to be between $1 million and $2 million– with the most likely settlement amount being $1.25 million.

IAS 37 defines and specifies the accounting for and disclosure of provisions, contingent liabilities, and contingent assets.

The measurement requirement refers to the company’s ability to reasonably estimate the amount of loss.

The journal entry would include a debit to legal expense for $1.25 million and a credit to an accrued liability account for $1.25 million.

What are some examples of contingent liabilities?

For example, Sierra Sports has a one-year warranty on partrepairs and replacements for a soccer goal they sell. Sierra Sports notices that some of its soccergoals have rusted screws that require replacement, but they havealready sold goals with this problem to customers. There is aprobability that someone who purchased the soccer goal may bring itin to have the screws replaced. Not only does the contingentliability meet the probability requirement, it also meets themeasurement requirement. A provision is measured at the amount that the entity would rationally pay to settle the obligation at the end of the reporting period or to transfer it to a third party at that time.

2 Recognition of provisions

The amount that the company should accrue is either the most accurate estimate within a range or– if no amount within the potential range is more likely than the others– the minimum amount of the range. A contingent liability is a potential obligation that depends on the occurrence or non-occurrence of one or more events in the future. If the event occurs, the company a contingent liability that is probable and for which the dollar amount can be estimated should be may be required to make a payment; if it does not occur, the company will not be required to make a payment. An automobile guarantee or other product warranties are examples of contingent liabilities that, are usually recorded on a company’s books.

Contingent Liabilities: Explanation

Similarly, the guidance in ASC 460 on accounting for guarantee liabilities, which has existed for two decades, is often difficult to apply because the determination of whether an arrangement constitutes a guarantee is complex. By 31 December 20X9, when Rey Co is required to make the payment, the liability should be showing at $10m, not $9.09m. Therefore, the liability is increased by 10% over the year, giving an increase of $910k which would be recorded in finance costs. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

If only one of the conditions is met, the liability must be disclosed in the footnotes section of the financial statements to abide by the full disclosure principle of accrual accounting. Some common examples of contingent liabilities are pending lawsuits and product warranties because each scenario is characterized by uncertainty, yet still poses a credible threat. The recognition of contingent liabilities on the financial statements (and footnotes) is to present investors, lenders, and others with reliable financial statements that contain accurate, conservative information.

At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. 11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. 11 Financial’s website is limited to https://www.bookstime.com/articles/accounting-for-amazon-sellers-amazon-bookkeeping the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links. Finally, during 2019, the company incurred $35,000 of warranty expenditures related to these printers.

Accrual for Contingent Liabilities

In May 2020 the Board issued Onerous Contracts—Cost of Fulfilling a Contract.

Consequently, the provision will increase each year until it becomes $20m at the end of the asset’s 25-year useful life.

Liquidity and solvency are measures of a company’s ability to pay debts as they come due.

These are questions businesses must ask themselves when exploring contingencies and their effect on liabilities.

Similar to the concept of a contingent liability is the concept of a contingent asset. Like a contingent liability, a contingent asset is simply disclosed rather than a double entry being recorded. Again, a description of the event should be recorded in addition to any potential amount. The key difference is that a contingent asset is only disclosed if there is a probable future inflow, rather than a possible one. The table below shows the treatment for an entity depending on the likelihood of an item happening. Google, a subsidiary of Alphabet Inc., https://x.com/BooksTimeInc has expanded from a search engine to a global brand with a variety of product and service offerings.

Now assume that a lawsuit liability is possible but not probable and the dollar amount is estimated to be $2 million.

Both represent possible losses and both depend on some uncertain future event.

Following are the necessary journal entries to record the expense in 2019 and the repairs in 2020.

IFRS Sustainability Standards are developed to enhance investor-company dialogue so that investors receive decision-useful, globally comparable sustainability-related disclosures that meet their information needs.

For a financial figure to be reasonably estimated, it could be based on past experience or industry standards (see Figure 12.9).

Application of Likelihood of Occurrence Requirement

IFRS Accounting Standards are, in effect, a global accounting language—companies in more than 140 jurisdictions are required to use them when reporting on their financial health. On that note, a company could record a contingent liability and prepare for the worst-case scenario, only for the outcome to still be favorable. The factor of uncertainty, where the outcome is out of the company’s control for the most part, is one of the core attributes of contingent liabilities.

This in turn means you can be far more efficient when it comes to collecting your payments. This ratio tells you how many times you’re collecting your what is the meaning of a favorable budget variance average accounts receivable balance. A higher ratio means that a company is collecting its receivables more quickly, which is a good thing.

Example of Accounts Receivable

It involves a range of tasks like onboarding new customers, evaluating their creditworthiness, issuing invoices on time, and timely collection of payments.

Any time a company has provided goods or services and the customer has purchased on credit or has an account still owing, this is considered the company’s Accounts Receivable.

CEI assesses collections efficiency over both regular intervals and long periods of time.

Although businesses have the option to write off uncollectible debt, it’s still better to select customers with a proven track record of positive debt repayment.

They can also choose to offer different payment options if credit is denied.

He has experience as an editor for Investopedia and has worked with the likes of the Consumer Bankers Association and National Venture Capital Association.

Poor communication can manifest in several ways, such as sending invoices that lack proper documentation or go to the wrong contact. To AR teams, it can look like a check that was “lost in the mail,” unexplained short payments, or payments sent with incomplete remittance information. Electronic billing and payment systems can help centralize and resolve invoicing and payment matters with your clients. For example, you can set automatic follow-ups with clients the first day a payment is late, then once each week until the account is settled. Jami Gong is a Chartered Professional Account and Financial System Consultant.

ways to improve receivables management

Intuit Inc. does not have any responsibility for updating or revising any information presented herein. Accordingly, the information provided should not be relied upon as a substitute for independent research. Intuit Inc. does not warrant that the material contained herein will continue to be accurate nor that it is completely free of errors when published.

Accounts payable is a current liability on the balance sheet, while accounts receivable is a current what is an accounts receivable ledger asset. If your accounts receivable balance is going up, that means you’re invoicing more. If the balance is going down, that means you’re collecting customer payments from previous invoices. Accounts receivable (AR) is an accounting term for money owed to a business for goods or services that it has delivered but not been paid for yet.

Even though it is not yet in hand, it is considered an asset because the company expects to receive it in due course. The shorter the period of time a company has accounts receivable balances, the better, as it means the company can use that money for other business purposes. The cash application process—a core tenet of accounts receivable management—is notoriously difficult, so most AR teams have a lot of room for improvement. Companies get paid faster when customers can have transparent access to their account, view invoice statuses, and easily make online payments.

What is accounts receivable? How to manage in 2024

If you use paper billing, you can still automate your communications to save time and streamline your process a little. Use integration software like Zapier to set up triggers to contact clients based on inputs into your records. For example, set up a form email to send to a client when you enter into a spreadsheet that you’ve received a payment. You can effectively manage increased orders and payment processing through online tools, while self-serve options can reduce the need for additional customer support members. Accounts Receivable Open, or AR Open, measures how many ongoing Accounts Receivable a business has in a given period. Closing Accounts Receivable translates to more payments being resolved; having Accounts Receivable remain open indicates ongoing disputes, unpaid invoices, or attempts to resolve bad debt.

What Are Net Receivables?

Accounts receivable represents money that a business is owed by its clients, often in the form of unpaid invoices. « Receivable » refers to fact that the business has earned the money because it has delivered a product or service but is, at that point in time, still waiting to receive the client’s payment. Clear communication is critical to an optimized collections process and good customer experience.

Compare traditional and modern Accounts Receivable tools to see how automating your Accounts Receivable processes knowing your debits from your credits can increase accuracy and efficiency. Good cash reconciliation can also improve a business’s customer relations. In the event of a dispute, having accurate records can back up your claims and help resolve disputes quickly and effectively.

I had a complicated set of onjectives, and they are helping me through all of them.

Create your username and password

1-800Accountant’s payroll experts work to make sure that the business stays IRS-compliant throughout the payment cycle. Automated payment systems also ensure that the payment process runs seamlessly every time. After scheduling a call with one of 1-800Accountant’s tax planning experts, users will be invited to actually sign up for an account on the platform. Getting started with 1-800Accountant involves following an onboarding/signup section with one of their expert account managers. In order to go through this process, users need to click on the online signup widget which then redirects towards a calendar booking form.

She holds a Bachelor’s degree from UCLA and has served on the Board of the National Association of Women Business Owners.

With a score of 4.8 out of 5, 1-800Accountant offers a robust range of features.

It’s our goal to provide personalized and competent service to help your business thrive.

Deciding on the right business phone system for your company can take a lot of research.

Every new client gets a dedicated accountant and those who sign up for more advanced plans can get access to advanced financial report preparation.

Small Business Payroll

All complaints are handled by the BBB where the company is Headquartered or a central customer complaint processing location. As a matter of policy, BBB does not endorse any product, service or business. Businesses are under no obligation to seek BBB accreditation, and some businesses are not accredited because they have not http://o-site.spb.ru/race.php?id=051015_mar sought BBB accreditation. Focus on running your business, and let us handle your day-to-day accounting. No contract or commitment is required with the 1-800Accountant business formation services. We sometimes offer premium or additional placements on our website and in our marketing materials to our advertising partners.

800Accountant Features

1-800 Accountant is an online accounting service that offers small business owners tax, bookkeeping and payroll services powered by CPAs. It features flat-rate monthly pricing so business owners know what to expect. Business owners get matched to a CPA with experience in their state and their industry. 1-800Accountant offers a diverse menu of services that include small business taxes and advisory, bookkeeping and payroll, and assistance with entity formation. Hi Anisha,Thank you for sharing your wonderful experience! We’re thrilled to hear that your onboarding calls have gone smoothly and that Perfect, your tax advisor, has been amazing.

Comparison To Other Services

The cost can vary widely based on what services are being used and the size of the business. There are four main packages offered, with each billed annually. If none of the packages meet a company’s needs, they can also create a customized package by working directly. Before a business is even formed, there are a variety of tasks an entrepreneur must complete. 1-800Accountant handles all legal documentation for entity formation, including filing for a tax ID and ensuring all assets are handled properly. Experts can also consult with businesses on the right structure for their business and how to minimize early tax burdens.

Clients appreciate the prompt and timely handling of their accounting and tax needs, from initial setup to ongoing management. The specialized software claimed to streamline accounting processes was not as user-friendly as expected, complicating rather than simplifying my accounting tasks. A separate area for Tax Projections provides a breakdown of taxable income and potential credits, as well as suggestions from a tax advisor to maximize returns and efficiency. For those who prefer to use a mobile device, both iOS and Android offer a mobile application that replicates web-based capabilities. All of the same features are available through the app, but the website is also optimized for mobile to be used on a browser.

Having engaged with 1-800Accountant for my business needs, I can attest to their comprehensive services. However, a drawback I noticed was a lack of transparency regarding their registered agent services. Customers consistently praise their responsive and knowledgeable support http://vverh-tatarstan.ru/news/2016.10.14/Alabuga-snova-priznana-luchshei-OEZ-v-Evrope/328 team, highlighting the company’s commitment to providing excellent service. Although 1-800Accountant promotes a personalized CPA matching service, my interaction was more generic than expected, lacking the industry-specific insight I anticipated based on their claims.

Partners may influence their position on our website, including the order in which they appear on a Top 10 list. Partners may influence their position on our website, including the order in which they appear on the page. Despite 1-800Accountant’s promise of efficiency, my request for tax advisory took longer than the advertised timeframe, highlighting a discrepancy in service delivery speed.

800Accountant Customer Support

We’re thrilled to hear that you found the initial call helpful and that our accountant provided valuable guidance. We’re here to support you every step of the way with your bookkeeping. Terrible experience over a whole tax year, involving almost $20,000 in wasted fees, penalties, https://evrazia-vladimir.ru/novinki/v-saydovskoi-aravii-postroiat-zavod-hyundai.html and over-taxation if I had not caught some of it. I should not have had to show them how to do their job (I’m not supposed to know how to do any of this). Even with my corrections, I still had $550 in health insurance premiums that were never deducted properly.

Annual subscriptions start at $139 monthly, and if you need help setting up your business, there are entity formation services available for an additional fee. Bookkeeping services start at $399 monthly and one major drawback is that they are only available with the Enterprise plan, which also includes priority support and access to financial reports. Hello Michael,Thank you for sharing your experience with us. We sincerely apologize for the long hold times and lack of follow-up from our team.

The benefit is that with long production chains involving multiple business entities you tax the places proportionally to how much they earn from that production chain. Now, you are arguing on a different system where this tax is not to your liking. This is a political choice and up to you to vote and promote other sources of government revenue.

This makes selecting a software solution tailored to your unique requirements crucial.

Now, you are arguing on a different system where this tax is not to your liking.

Registering requires them to pay this tax even though they shouldn’t have to.

Most tax regimes try to account for this, by incorporating a tax-free amount that’s supposed to represent the amount need to maintain a basic lifestyle.

Zoho Books is perfect for freelancers who need comprehensive accounting software that is easy to use and affordable.

One of the standout features of Invoicely is its automation capabilities, which can save time and reduce errors by automating recurring invoices, payment reminders, and late fees.

FreshBooks

Opponents of the New York rule argue that because some lawyers may be unable to make prompt refund of unearned retainers, all lawyers should be required to escrow advance retainers and withdraw their fees only after a bill has been rendered. Larger businesses might exert pressure on small businesses to cut the price of transactions to match what would have been paid back in consumption tax. Now really really, freelancers should be like « We are going to charge consumption tax so are increasing the tax inclusive amount by 10%. Please deduct things correctly » to businesses. B2B interactions are already basically marketed at tax exclusive rates. Consumption tax is a tax added to the purchase of goods and services, and is usually paid by the consumer, but at this time, the « consumption tax amount on purchases » is deducted from the « consumption tax amount on business sales ». The bookkeeping method calculates this purchase tax credit based on the business’s books.

– Freelancers aren’t happy with Japan’s new invoice system

The money origins from the government (it says as much on the bills, even has a signature), and the only way to make anybody actually want that money is to force them to pay it to the government. If you work for a living you have to pay taxes in the government money – so naturally you’ll want your wages in government money. We offer professional, personalized service at prices that entrepreneurs and small businesses can afford.

Choosing the Right Invoicing Software for Your Freelance Business

I already paid taxes on my income, now I need to pay additional taxes on what I consume…why? Kindly note here that I’m not arguing against the concept of paying taxes, but against the fact of being taxed on both income and outgoings. Sure, you might need that BMW to « drive to work » but obviously a significant fraction of that car’s purchase price isn’t for « the sake of maintaining their job ». Even a benchmark of « cheapest sedan you can buy » is tricky, because you can take public transit (depending on where you live), buy used, carpool, or bike. Where do you draw the line between necessity and paying a premium for a better experience (ie. consumption)?

Software vendors

The PO is an agreement that creates a binding contract between the two parties. Both the purchase order and the invoice should match on all terms, including price. An invoice is an itemized bill for goods or services to be paid at a later time. Note the word “itemized,” meaning that each item on the bill or each charge is listed separately. Also, note that the invoice includes information on when the customer must pay (more on this later). The new invoice system will affect a wide range of workers from freelancers to taxi drivers who work independently and not for a taxi company.

He says that offering several methods of payment provides more flexibility for the clients.

He discusses payment and credit terms upfront when his firm first takes on a job.

Thankfully, invoicing software can streamline the billing process and offer other benefits to manage, automate, and organize your business.

(Of course, govt revenue will increase temporarily whenever taxes increase.) Most of the highest tax nations have mediocre national output.

Because in absence of it companies could just keep their prices as high as they are (because why lower them if the customer already pays them) while keeping all that money.

FreshBooks is cloud-based, making it a great solution for freelancers to manage their finances on the go. FreshBooks also offers a mobile app for iOS and Android devices, allowing busy freelancers to manage their finances from smartphones or tablets. The software is easy to set up and use, with a simple and intuitive interface. With FreshBooks, users can streamline their invoicing and accounting processes, allowing them to focus on growing their business. Invoicely is a versatile invoicing software platform designed to cater to the freelancers aren happy new invoice system needs of freelancers and small businesses.

This risk might occur even if the lawyer had fully earned the advance retainer and was credit-worthy throughout the representation. Navigating the world of invoicing software can be overwhelming, with countless options vying for your attention. This section will review the top invoice software solutions designed for freelancers. We’ll cover each platform’s key features, pros, and cons, so you can confidently choose the one that best aligns with your https://www.bookstime.com/ business needs and workflow.

What if ItalyCorp decides they are not an Italian company, but actually a company based out of the Canary Islands in no way bound to Italy?

QuickBooks Online provides various pricing plans, including a free trial, to cater to businesses of different sizes and needs.

Learn how to handle your security deposit as a tenant with deposit invoice templates.

In 1994, Matter of Cooperman 83 NY2d 465, 611 NYS2d 465 (1994), invalidated retainer agreements providing for non-refundable retainer fees.

Create your username and password

Invoicely also offers https://x.com/BooksTimeInc customizable invoice templates tailored to fit a business’s brand and style. The software also allows easy integration with payment gateways like PayPal and Stripe, allowing freelancers to accept online payments. Another key feature is the ability to track expenses and generate financial reports, providing a comprehensive view of a business’s financial health. Wave is a popular invoicing software solution that caters to freelancers and small businesses looking for a cost-effective way to manage their finances. With its user-friendly interface and robust set of features, Wave simplifies the invoicing process and helps freelancers stay organized and professional. Moreover, until billed and withdrawn from the lawyer’s trust account, any advance fee payments in a criminal representation would be subject to asset-freeze or forfeiture orders.

Small businesses fret as start of new invoice system looms

Proponents of a new advance fee escrow rule would require lawyers to remove funds from escrow only after they render a “reasonably detailed” bill to the client for services actually rendered. In a typical criminal defense representation, these requirements could prove devastating to the client. Billing statements are unsung heroes of business transactions that document details of a financial transaction between a buyer and a seller. They provide a record of transactions for accounting purposes, facilitate the tracking of payments and outstanding balances, and represent the foundation for better financial decision-making.